Hidden Knowledge

Bluffing, Signalling, and Asymmetric Information

When you do not know what the other player wants, every action becomes a clue — and the costliest clues are the most credible.

In 2005, a twenty-six-year-old named Matt recently graduated from a mid-tier university applied for a software engineering position at Google. His résumé was unremarkable — decent GPA, no elite internships, no publications. He was rejected without an interview. Two years later, having spent nights and weekends contributing to a prominent open-source project — writing code that anyone could inspect — he reapplied. This time, Google flew him to Mountain View. The open-source contributions cost Matt hundreds of hours of unpaid labor. They didn't teach him anything he couldn't have learned faster in a paid job. But they solved a problem that no résumé bullet point could: they proved, in a way that was extraordinarily costly to fake, that he was genuinely talented.

Matt's story captures the central puzzle of this chapter. In every game we've analysed so far, players knew each other's payoffs. A firm knew its rival's cost structure. A prisoner knew exactly how much the other prisoner valued freedom versus loyalty. That assumption — complete information — was convenient, and it let us develop powerful tools. But it was a lie. In most strategic situations that matter, you don't know what the other player truly wants, what they're capable of, or what they're willing to endure. You must infer it. And they know you're trying to infer it. Welcome to the world of incomplete information.

Complete vs. Incomplete Information

Let's be precise about what we're breaking. In Chapters one through six, we operated under an assumption so pervasive it was almost invisible: every player knew the full structure of the game — all the strategies, all the payoffs, for all the players. This is complete information. Note that this is different from perfect information, which we discussed in Chapter two. Perfect information means you can observe every move that has been made before choosing your own, as in chess. Complete information means you know what every player wants — you know their utility functions. A game can have complete but imperfect information, like a simultaneous-move game where you know payoffs but not your opponent's choice, or incomplete information, where you don't know some player's payoffs at all.

Think about the difference. When you play rock-paper-scissors, you can't observe your opponent's choice — that's imperfect information — but you know they prefer winning to losing to drawing — that's complete information. Now imagine playing a negotiation game against someone, and you don't know whether they're a tough bargainer who would rather walk away than accept a bad deal, or a desperate seller who would accept almost anything. That is incomplete information. Their preferences — their type — are hidden from you.

Why does this matter strategically? Because when you don't know someone's type, every action they take becomes a potential clue. If the seller rejects your low opening offer, does that mean they're genuinely tough, or are they bluffing? If a job candidate has a PhD, does that mean they're brilliant, or did they simply have the patience to endure graduate school? Incomplete information turns every game into a detective story, and in this chapter, we'll develop the tools to read the clues.

Harsanyi's Revolution · Nature as a Player

For decades, the problem of incomplete information seemed analytically intractable. If Player one doesn't know Player two's payoffs, then Player one doesn't know what game they're playing. And if Player one doesn't know what game they're playing, how can we define equilibrium? John Harsanyi's breakthrough, published across three landmark papers, as Harsanyi showed in 1967, was elegant in its simplicity: introduce a fictitious player called Nature.

Here's how it works. Before the game begins, Nature moves first, randomly assigning each player a type from some set of possible types. Each player observes their own type but not the types of the other players. Crucially, the probability distribution over types — the chances that Nature assigns any particular type — is common knowledge. Everyone knows the distribution; they just don't know the realisation.

This is a subtle but profound move. Consider an insurance market. An applicant knows whether they are a safe driver or a reckless one. The insurance company doesn't know this specific applicant's type, but it knows the population distribution: perhaps seventy percent of applicants are safe and thirty percent are reckless. By modelling "Nature assigns the applicant a type — safe with probability zero point seven, reckless with probability zero point three," Harsanyi converted a game of incomplete information into a game of imperfect information. And games of imperfect information — games with information sets, like we studied in Chapter two — we already know how to analyse.

The resulting game is called a Bayesian game, and the equilibrium concept is Bayesian Nash equilibrium: a strategy profile where each type of each player is maximising their expected payoff, given their beliefs about the distribution of other players' types, as Gibbons described in 1992. It's Nash equilibrium, but with an extra layer — you're optimising not against a known opponent, but against a distribution of possible opponents.

Bayesian Updating · Reading the Clues

If the other player's type is hidden, how do you learn anything about it? The answer is Bayesian updating — the process of rationally revising your beliefs when you observe new evidence. You begin with a prior belief, your initial probability estimate about the other player's type, you observe an action or signal, and you use Bayes' rule to compute a posterior belief — your updated probability given what you've seen.

The mathematics are straightforward. Suppose you think there's a forty percent chance your opponent is Type H, high, and a sixty percent chance they're Type L, low. You observe them take some action — say, investing heavily in advertising. You know that Type H firms advertise with probability zero point nine, while Type L firms advertise with only probability zero point three. Bayes' rule says: the probability of H given advertise equals the probability of advertise given H times the probability of H, divided by the quantity the probability of advertise given H times the probability of H plus the probability of advertise given L times the probability of L.

Plugging in: the probability of H given advertise equals zero point nine times zero point four, divided by zero point nine times zero point four plus zero point three times zero point six, which equals zero point three six divided by zero point five four, approximately zero point six six seven. Your belief that they're Type H jumped from forty percent to sixty-seven percent. The action carried information because it was much more likely to come from a Type H player.

Notice the critical insight: the informativeness of a signal depends on how differently the two types behave. If both types advertise with equal probability, observing advertising tells you nothing — your posterior equals your prior. If only Type H ever advertises, then observing advertising tells you everything — your posterior jumps to one hundred percent. The greater the gap in behaviour between the types, the more informative the signal. This connects directly to our work on mixed strategies in Chapter four: when a player randomises, their actions become partially informative rather than fully revealing, as Fudenberg and Tirole noted in 1991.

The key intuition: seeing a raise should make you think they're less likely to be bluffing, because strong hands raise even more often than bluffers do. The posterior is zero point eight times zero point five, divided by zero point eight times zero point five plus zero point nine five times zero point five, which equals zero point four divided by zero point eight seven five, approximately zero point four five seven. A small shift, because both types raise frequently — the signal is noisy.

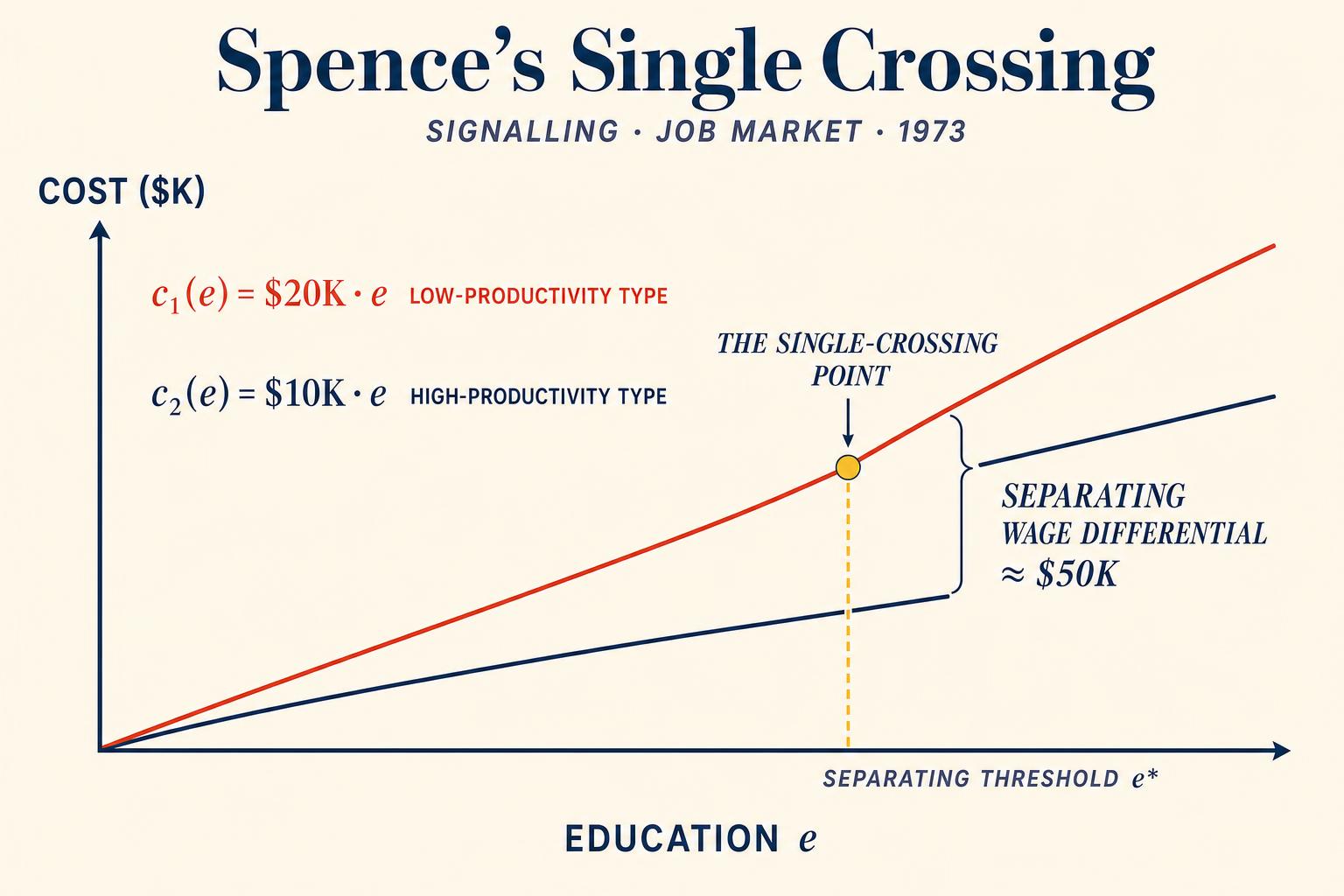

Spence's Signalling Model · Education as a Signal

Bayesian updating tells us how to read signals. But who sends them, and why? This is the domain of signalling theory, and its most famous model comes from Michael Spence's analysis of the job market, as Spence presented in 1973.

Consider a labour market with two types of workers: high-ability, H, and low-ability, L. A high-ability worker produces output worth one hundred thousand dollars to a firm; a low-ability worker produces fifty thousand dollars. Workers know their own type, but employers cannot directly observe ability. If the employer simply offers the average wage — say, seventy-five thousand dollars if the population is evenly split — high-ability workers are underpaid and low-ability workers are overpaid. This is a pooling outcome, and it creates a problem: high-ability workers want to distinguish themselves.

Enter education. In Spence's model — and this is the part that shocks students every time — education need not make workers more productive. It doesn't have to teach useful skills. It simply needs to be differentially costly. Specifically, suppose that getting a degree costs a high-ability worker thirty thousand dollars in effort, time, and foregone wages, but costs a low-ability worker sixty thousand dollars, because the coursework is harder for them, it takes longer, and so on. This difference in cost is called the single-crossing property.

The Separating Equilibrium · Math of a Costly Bluff

Now consider a potential separating equilibrium: employers believe that workers with degrees are Type H and those without are Type L, paying one hundred thousand and fifty thousand dollars respectively. Would either type want to deviate?

Type H gets a degree, cost thirty thousand dollars, earns one hundred thousand dollars. Net payoff: seventy thousand dollars. Without the degree, earns fifty thousand dollars. Net payoff: fifty thousand dollars. Type H prefers to get the degree.

Type L gets a degree, cost sixty thousand dollars, earns one hundred thousand dollars. Net payoff: forty thousand dollars. Without the degree, earns fifty thousand dollars. Net payoff: fifty thousand dollars. Type L prefers not to get the degree.

The equilibrium holds. Education separates the types not because it adds value, but because it's cheap for the talented and expensive for everyone else. The signal is credible for precisely the reason a threat is credible, recall Chapter five: it would be too costly to fake. The high-ability worker burns thirty thousand dollars to prove their type — a loss in absolute terms, but a gain relative to being pooled with low-ability workers.

The Pooling Alternative

The separating equilibrium isn't the only possibility. Consider a pooling equilibrium where both types choose the same education level — say, no education. If employers believe that education conveys no information, because everyone does the same thing, they offer the average wage of seventy-five thousand dollars to everyone. Would any type deviate? Only if getting a degree and being perceived as Type H, earning one hundred thousand dollars, is worth the cost. For Type H, deviating yields one hundred thousand minus thirty thousand equals seventy thousand dollars, which is less than seventy-five thousand dollars. For Type L, deviating yields one hundred thousand minus sixty thousand equals forty thousand dollars, which is also less than seventy-five thousand dollars. Neither type deviates, so this pooling equilibrium also survives.

Which equilibrium actually emerges? This is one of the deepest questions in signalling theory, and it depends on refinement criteria — ways of ruling out "unreasonable" beliefs. The intuitive criterion, developed by Cho and Kreps, argues that if the only type who could possibly benefit from deviating to a particular education level is Type H, then employers should believe the deviator is Type H, as Sobel reviewed in 2007. Under this refinement, many pooling equilibria collapse, and the separating equilibrium survives. The intuition is appealing: if only a talented worker would bother getting the degree, it's unreasonable for employers to ignore the degree.

The classic illustration of these refinements is the beer-quiche game: a "tough" or "wimpy" type chooses breakfast, a bully observes the choice and decides whether to pick a fight, and both pooling and separating equilibria exist depending on what off-path beliefs we permit. The intuitive criterion sweeps away the equilibria where bullies attack quiche-eaters — because no genuinely tough type would prefer quiche to beer if it invited a beating, so observing beer should not be read as cowardice.

Why Costly Signals Travel Across Disciplines

Think about real-world signals that work like Spence's education model — not primarily because of what they teach, but because of what they prove about the person willing to endure them. Consider military boot camp, unpaid internships, marathon running, writing a PhD dissertation. What makes each costly, and why is that cost harder to bear for the "wrong" type?

Spence's logic extends far beyond education. As Riley surveyed in 2001, twenty-five years of applications span economics and biology. Consider peacock tails: the classic biological analogue. A male peacock's extravagant tail plumage is metabolically expensive to grow and makes him more vulnerable to predators. Only a genuinely fit peacock can afford the handicap. The tail signals genetic quality to potential mates — it's credible precisely because it's wasteful.

Luxury spending is another example. Thorstein Veblen's "conspicuous consumption" is signalling theory before the formal theory existed. Buying a ten-thousand-dollar watch that tells time no better than a fifty-dollar one signals wealth. The signal works because only the genuinely wealthy can afford to burn money like this without suffering.

Startup funding rounds follow the same pattern. When a venture capital firm leads a Series A round at a high valuation, it signals confidence in the startup to later-round investors. The VC's investment is costly — if the startup fails, the money is lost. The willingness to risk capital is the signal.

Product warranties work similarly. A firm offering a ten-year warranty on its product signals high quality. If the product were likely to break, the warranty would be ruinously expensive. Low-quality firms can't afford to offer the same terms.

In every case, the structure is identical: a privately-informed party takes a costly action that is differentially costly by type, and an uninformed party updates their beliefs accordingly. The signal works not in spite of its cost, but because of it.

Screening · Menus that Make You Reveal Yourself

In signalling, the informed party, the worker, moves first, choosing an action that reveals their type. But what if the uninformed party moves first instead? This is screening, and the distinction matters more than it might seem, as Cho and Kreps showed in 1987.

In a screening model, the uninformed party designs a menu of options — a set of contracts — designed so that each type self-selects into the contract intended for them. The classic example is insurance, developed formally by Rothschild and Stiglitz in 1976. An insurance company cannot observe whether you're a safe or reckless driver. But it can offer you a choice: Option A, high premium, low deductible, full coverage. Option B, low premium, high deductible, basic coverage.

The key insight: reckless drivers, who expect to file claims frequently, prefer full coverage even at a higher premium. Safe drivers, who rarely file claims, prefer to save on premiums and accept a higher deductible. The menu is designed so that each type voluntarily reveals themselves through their choice. Nobody is forced to disclose anything — the menu structure does the work. This is sometimes called self-selection or incentive-compatible contract design.

The asymmetry between signalling and screening is about who bears the cost of information revelation. In signalling, the informed party pays — the worker buys education. In screening, the uninformed party designs the mechanism, and the "cost" is borne through distortion — the insurance company must offer the safe type an imperfect contract, with a higher deductible than they'd get under full information, to prevent the reckless type from mimicking them. As Riley emphasised in 2001, in signalling games, all contracts break even in equilibrium, while screening games can sustain cross-subsidisation between types.

Cheap Talk · When Words Are Free

Not all communication is costly. Politicians make campaign promises. Job applicants describe themselves as "hardworking." Friends recommend restaurants. These messages are cheap talk — they're costless to send, regardless of whether they're true, as Crawford and Sobel showed in 1982.

The central question of cheap talk theory is: can costless messages convey any information at all? If messages are free, why wouldn't every type send the most favourable message? A low-ability worker could say "I'm high-ability" just as easily as a high-ability worker. The signal has zero differential cost — the single-crossing property fails completely.

Crawford and Sobel's 1982 seminal model shows that the answer depends on how aligned the players' interests are. If the sender and receiver have identical preferences — they both want the receiver to take the action that's optimal given the true state — then the sender has no incentive to lie, and cheap talk can be fully informative. But when interests diverge, the sender has an incentive to shade the truth, and the receiver, knowing this, discounts the message. The result is partial information transmission at best.

In Crawford and Sobel's framework, the degree of information transmission is inversely related to the degree of interest conflict between sender and receiver. When preferences are perfectly aligned, talk is cheap but honest. When they're diametrically opposed, talk is truly just babble.

Sobel, 2007

Consider some examples. A restaurant review from a friend with similar tastes is informative cheap talk — your interests are aligned, so they have little reason to mislead you. A car salesman's claim that "this is the best deal in town" is much less informative — his interest, selling at a high price, conflicts with yours, buying at a low price. A politician's promise to "fight for working families" is perhaps the purest form of cheap talk — costless, vague, and sent by every type regardless of true intent.

An important result from Crawford and Sobel: babbling equilibria always exist. A babbling equilibrium is one where the sender sends random messages, and the receiver ignores all messages. This is always a Nash equilibrium of a cheap talk game because, if the receiver ignores messages, the sender is indifferent about what they say, and if the sender babbles, the receiver is right to ignore them. The existence of babbling equilibria underscores a key point: unlike costly signals, which are credible by construction, cheap talk messages are only informative if both parties tacitly agree to make them so.

Three Categories · Signalling, Screening, Cheap Talk

We now have three fundamental categories for understanding how information moves, or fails to move, between players with asymmetric information.

First, signalling. The informed party moves first, taking a costly action that reveals their type. Credibility comes from differential cost, the single-crossing property. Examples include education, product warranties, and venture capital investment.

Second, screening. The uninformed party moves first, offering a menu that induces self-selection. Credibility comes from incentive-compatible design. Examples include insurance deductible menus, airline ticket classes such as business versus economy, and volume discounts.

Third, cheap talk. Costless messages that may or may not carry information, depending on preference alignment. Examples include political promises, pre-play communication in coordination games, and job interview claims.

These categories connect deeply to concepts from earlier chapters. A signal is credible for the same reason a commitment is, recall Chapter five — it involves a real cost that the wrong type wouldn't bear. Screening relies on backward induction, Chapter three — the uninformed party reasons backward from the types' incentives to design the optimal menu. Bayesian updating requires the probabilistic reasoning we developed with mixed strategies in Chapter four. And the information sets from Chapter two provide the formal representation: when the employer cannot distinguish between a high-ability and low-ability worker, those two nodes sit in the same information set.

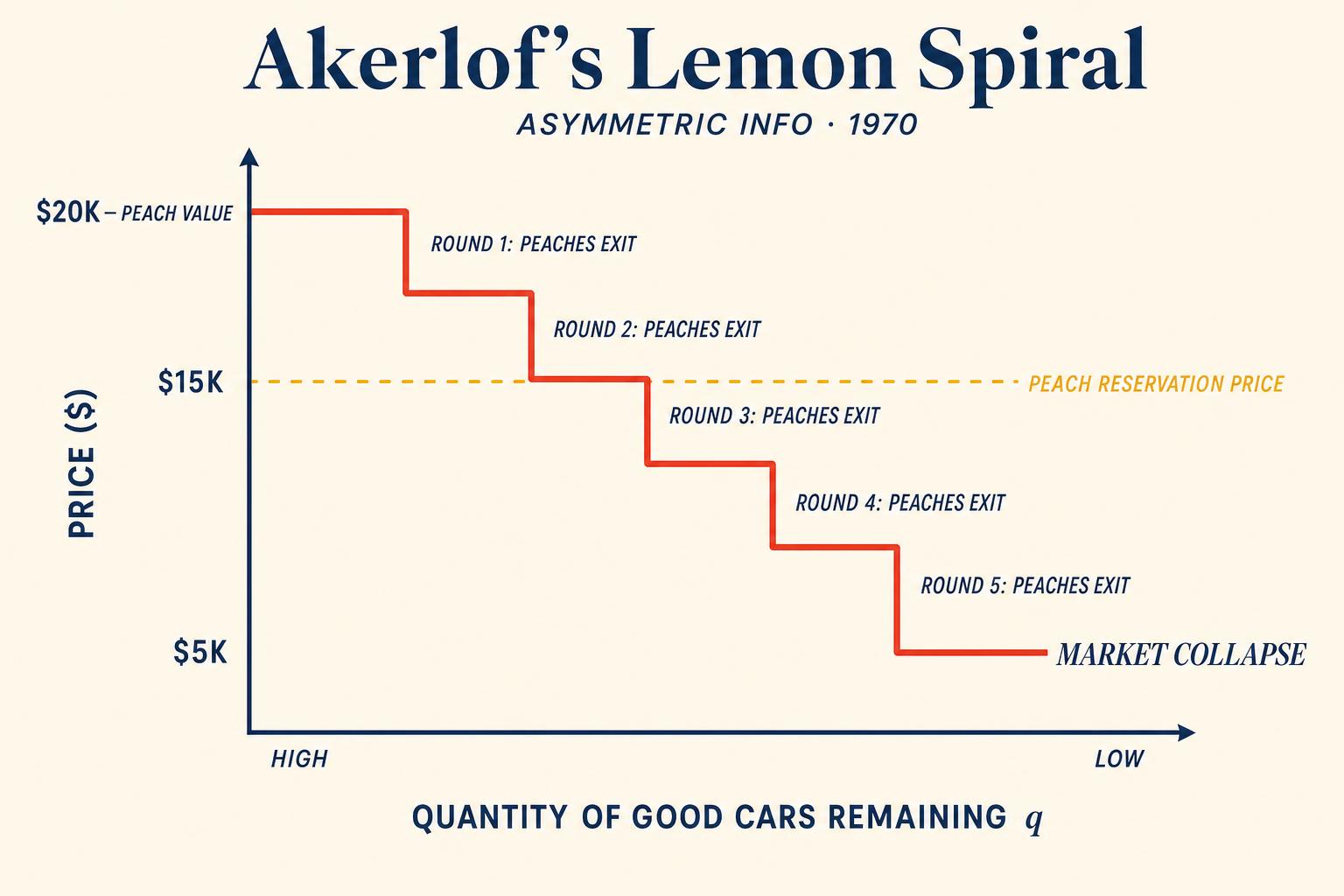

The Market for Lemons · How Asymmetry Kills Markets

The concepts in this chapter aren't merely theoretical curiosities. Information asymmetry can cause entire markets to unravel. George Akerlof's famous Market for Lemons, published in 1970 and which we'll formalise more fully later in the course, shows that when buyers can't distinguish high-quality from low-quality sellers, the average price falls, high-quality sellers exit, and the market may collapse entirely. Signalling, screening, and even cheap talk are all mechanisms that societies develop to fight this unravelling.

Universities exist partly as signalling institutions. Insurance companies invest billions in screening mechanisms. Professional certifications, brand reputations, online review systems, money-back guarantees — all of these are responses to the fundamental problem Harsanyi formalised: players don't know each other's types, and that ignorance has strategic consequences.

The framework also illuminates some counterintuitive policy implications. If education primarily serves as a signal rather than building human capital, then subsidising education might increase the total amount of signalling without increasing total productivity — everyone gets more education, but the relative ranking stays the same. This is the signalling arms race, and it suggests that the social return to education may be lower than the private return. Whether education is primarily a signal or primarily human capital accumulation remains one of the most important — and most contested — questions in labour economics.

Bayesian Nash Equilibrium · Formal Machinery

Let's consolidate the formal machinery. A Bayesian game consists of, as Fudenberg and Tirole described in 1991 and Gibbons in 1992: a set of players; a set of types for each player; a common prior probability distribution over types; a set of actions for each player; and payoff functions that depend on actions and types.

A Bayesian Nash equilibrium is a strategy profile where each type of each player is maximising their expected payoff given their beliefs about other players' types and the strategies those types play.

In a signalling game, a dynamic Bayesian game, we use a stronger concept: perfect Bayesian equilibrium, or PBE. A PBE requires not only that strategies are sequentially rational, optimal at every information set, but also that beliefs are derived from Bayes' rule wherever possible. When a player observes an action that was supposed to have zero probability in equilibrium, an "off-path" action, Bayes' rule doesn't apply, and additional refinements — like the intuitive criterion — restrict what beliefs are "reasonable."

Key Takeaways

- Incomplete information means players don't know each other's payoffs. Harsanyi's framework (1967–68) converts this into imperfect information by introducing Nature, who assigns types according to a known probability distribution.

- Bayesian updating, using Bayes' rule, is the rational process for revising beliefs after observing actions. A signal is more informative when the two types behave more differently.

- In Spence's (1973) signalling model, costly actions like education can reveal private information even if they have no direct productive value. The key is the single-crossing property: the signal must be differentially costly by type.

- Separating equilibria reveal types through different actions; pooling equilibria hide types behind identical actions. Equilibrium refinements like the intuitive criterion (Cho & Kreps; the beer-quiche game) help select among multiple equilibria.

- Screening (Rothschild & Stiglitz, 1976) flips the timing: the uninformed party designs a menu of contracts to induce self-selection — for example insurance deductibles.

- Cheap talk (Crawford & Sobel, 1982) involves costless messages that transmit information only when interests are partially aligned; babbling equilibria always exist.

- The credibility of a signal comes from its cost — the same logic as credible commitments. A signal that's free to fake is no signal at all.

- Information asymmetry can cause market failures, as in Akerlof's (1970) market for lemons; signalling, screening, and reputation mechanisms are society's responses to the problem of hidden types.

In the next chapter we enter the world of auctions — and the signalling framework returns with a vengeance. In a common-value auction, every bidder is uncertain about the true value of the item, and each bid is a signal. The winner's curse — the phenomenon where the winning bidder has systematically overpaid — is a direct consequence of failing to properly Bayesian-update. We'll also see how auction design is fundamentally a screening problem: the seller designs the rules, the menu, and bidders self-select through their bids.

References

Akerlof, G. A. (1970). The market for "lemons": Quality uncertainty and the market mechanism. The Quarterly Journal of Economics, 84(3), 488–500.

Cho, I.-K., & Kreps, D. M. (1987). Signaling games and stable equilibria. The Quarterly Journal of Economics, 102(2), 179–221.

Crawford, V. P., & Sobel, J. (1982). Strategic information transmission. Econometrica, 50(6), 1431–1451.

Fudenberg, D., & Tirole, J. (1991). Game theory. MIT Press.

Gibbons, R. (1992). Game theory for applied economists. Princeton University Press.

Harsanyi, J. C. (1967–68). Games with incomplete information played by Bayesian players (Parts I–III). Management Science, 14(3, 5, 7).

Riley, J. G. (2001). Silver signals: Twenty-five years of screening and signaling. Journal of Economic Literature, 39(2), 432–478.

Rothschild, M., & Stiglitz, J. (1976). Equilibrium in competitive insurance markets: An essay on the economics of imperfect information. The Quarterly Journal of Economics, 90(4), 629–649.

Sobel, J. (2007). Signaling games. In S. N. Durlauf & L. E. Blume (Eds.), The new Palgrave dictionary of economics. Palgrave Macmillan.

Spence, M. (1973). Job market signaling. The Quarterly Journal of Economics, 87(3), 355–374.