Going Once, Going Twice

The Surprising Science of Auctions

Four canonical formats, one revenue theorem, the bias that curses the winner, and the Nobel-winning design that turned spectrum into a hundred billion dollars.

On July twenty-five, nineteen ninety-four, a room full of telecommunications executives, flanked by teams of game theorists and consultants, sat before computer terminals in Washington, D-C. The Federal Communications Commission was about to do something no government had ever attempted at this scale: auction off slices of the electromagnetic spectrum — the invisible resource that carries every phone call, text message, and data stream. Over forty-seven grueling rounds, companies bid against one another in a format designed from scratch by economists Paul Milgrom and Robert Wilson. When the final gavel fell, the U-S Treasury was six hundred seventeen million dollars richer from that first narrowband auction alone, as Cramton reported in nineteen ninety-seven. Within a decade, spectrum auctions worldwide would generate over one hundred billion dollars.

These auctions did not succeed by accident. They succeeded because of a body of theory — developed over three decades by mathematicians and economists — that reveals the deep strategic logic governing how people compete for scarce goods. That theory is the subject of this chapter. By the end, you will understand why a peculiar auction format makes honesty your best strategy, why all standard auctions secretly generate the same revenue, why winning can be the worst thing that happens to you, and how abstract theorems became a policy tool worth tens of billions of dollars.

Four Formats, One Mechanism

An auction is a mechanism for selling goods where the price is determined by competitive bidding. That simple description conceals enormous strategic variety, because the rules of an auction — who bids when, who sees what, and how the winner pays — fundamentally alter the game that bidders play. Auction theory organizes this variety around four canonical formats, each of which appears in real markets around the world, as Krishna described in two thousand nine.

English Ascending

The English ascending auction is the format most people picture when they hear the word "auction." The auctioneer starts at a low price and calls out successively higher prices. Bidders signal their willingness to pay by remaining active — raising a paddle, nodding, or simply not withdrawing. As the price climbs, bidders drop out one by one. The last bidder standing wins the item and pays the price at which the second-to-last bidder withdrew. Christie's, Sotheby's, and most charity fundraisers use this format. So does eBay, in a modified online version.

The strategic logic is straightforward: you should stay in the bidding as long as the current price is below your valuation, and drop out the moment it exceeds what the item is worth to you. There is no reason to drop out earlier — you might miss a bargain — and no reason to stay in beyond your value — you would risk paying more than the item is worth. The outcome is efficient: the bidder who values the item most wins, and the price equals the second-highest valuation among all bidders.

Dutch Descending

The Dutch descending auction runs in the opposite direction. The auctioneer starts at a very high price and lowers it gradually — think of a large clock ticking downward. The first bidder to call out "Mine!" wins the item and pays the price at which they stopped the clock. The format gets its name from the Dutch flower markets in Aalsmeer, Netherlands, where millions of flowers are sold this way every morning.

The Dutch auction creates a genuinely different strategic problem. You see no information about other bidders' willingness to pay — no one has acted yet — so you must decide in advance at what price to claim the item. Bid too early, at a high price, and you overpay. Wait too long and someone else grabs it first. The tension between securing the item and getting a good deal is acute, and there is no dominant strategy in the way there is for the English auction.

First-Price Sealed-Bid

In a first-price sealed-bid auction, each bidder submits a single bid in a sealed envelope, or these days, electronically. The auctioneer opens all bids simultaneously, and the highest bidder wins, paying exactly what they bid. Government procurement contracts, mineral rights auctions, and many business-to-business transactions use this format.

Notice something: the strategic problem facing a bidder in a first-price sealed-bid auction is identical to that in a Dutch auction. In both cases, you must commit to a price without knowing what anyone else has bid. You face the same tension between bidding high to win and bidding low to profit. This strategic equivalence between the Dutch auction and the first-price sealed-bid is our first hint that apparently different auction formats can be deeply connected, as Levin noted in two thousand four.

Vickrey · Second-Price Sealed-Bid

The fourth format is the most elegant and, for students of game theory, the most instructive. In the Vickrey auction — named after the Columbia University economist William Vickrey, who analyzed it in his landmark nineteen sixty-one paper — each bidder submits a sealed bid. The highest bidder wins, but pays not their own bid, but the second-highest bid. This seemingly peculiar payment rule transforms the strategic landscape in a remarkable way.

Vickrey's Beautiful Theorem · Honesty as Dominant Strategy

William Vickrey's nineteen sixty-one paper, "Counterspeculation, Auctions, and Competitive Sealed Tenders," contains one of the cleanest results in all of game theory: in a second-price sealed-bid auction, bidding your true valuation is a weakly dominant strategy. This means that no matter what any other bidder does — no matter how many bidders there are, no matter what their strategies might be — you can never do better than bidding exactly what the item is worth to you. Let us construct the argument ourselves.

Suppose the item is worth v to you. You are considering what bid b to submit. After all bids are collected, let h denote the highest bid among all other bidders. You do not know h in advance, but you can reason through the possibilities.

Case one · You bid your true value, b = v

If h is less than v, you win and pay h, earning a surplus of v minus h, which is greater than zero. If h is greater than v, you lose, earning zero. If h equals v, you tie and earn zero surplus regardless.

Case two · You overbid, b > v

Compared to bidding v, overbidding only changes the outcome when h falls between v and b. In this range, bidding b causes you to win and pay h — but since h is greater than v, your surplus is v minus h, which is less than zero. You win the auction but lose money. In every other case, overbidding produces the same outcome as truthful bidding. So overbidding is weakly worse.

Case three · You underbid, b < v

Compared to bidding v, underbidding only changes the outcome when h falls between b and v. In this range, bidding v would have won you the item at price h, giving you positive surplus v minus h greater than zero. But because you underbid, you lose and get zero. In every other case, underbidding produces the same outcome. So underbidding is weakly worse.

This completes the argument. Bidding your true value is at least as good as any other bid in every scenario, and strictly better in some scenarios. It is a weakly dominant strategy — precisely the concept we developed earlier. Vickrey's payment rule, by decoupling what you bid from what you pay, eliminates any incentive to shade your bid or to bluff. The result is beautiful: a mechanism that makes honesty the strategic best response.

Notice the parallel with the English auction. In both formats, the bidder with the highest valuation wins and pays the second-highest valuation. The English auction achieves this through an open, dynamic process of elimination; the Vickrey auction achieves it through a clever payment rule applied to sealed bids. The two formats are strategically equivalent in the independent private values setting — a connection Vickrey himself identified, as noted by Levin in two thousand four.

A mechanism that makes honesty the strategic best response — Vickrey turned a peculiar payment rule into a fixed point of truthful behaviour.

after Vickrey, 1961

The Revenue Equivalence Theorem

Theory claims that English and Vickrey auctions are equivalent, and that Dutch and first-price sealed-bid auctions are equivalent. But how do these pairs compare to each other? If you could experience all four formats firsthand, bidding against AI opponents, after several rounds you would likely notice something remarkable: the seller's average revenue would be roughly the same across all four auction formats. This is not a coincidence. It is a deep theorem — one of the crown jewels of auction theory.

The Revenue Equivalence Theorem states that under a specific set of assumptions, any auction mechanism in which the item goes to the bidder with the highest valuation, and in which a bidder with the lowest possible valuation expects zero surplus, will yield the same expected revenue to the seller, as Myerson demonstrated in nineteen eighty-one. All four standard formats satisfy these conditions, and therefore all four generate the same expected revenue.

Revenue equivalence holds when bidders are risk-neutral, their valuations are independently drawn from the same probability distribution — that's called independent private values — and the auction allocates the item to the bidder with the highest valuation. Let us unpack why.

The intuition runs through what economists call the envelope theorem approach, as Milgrom described in two thousand four. A bidder's expected surplus in any auction depends only on two things: their probability of winning, which in equilibrium is the same across formats — the highest-value bidder always wins — and the information rent they extract from having a higher valuation than marginal competitors. Since the probability of winning is determined entirely by the distribution of valuations and the equilibrium allocation rule, and since the surplus of the lowest type is zero in all formats, the entire surplus schedule — and therefore the expected payment schedule — must be the same. What differs is the form of payment: you pay your own bid in first-price, you pay the second-highest bid in Vickrey, but the expected amount is identical.

This result is both powerful and fragile. It is powerful because it tells us that, under standard conditions, the choice of auction format is irrelevant for revenue — the seller can use whichever format is most convenient or transparent. It is fragile because violations of the assumptions — risk aversion, correlated values, asymmetric bidders, collusion — can break equivalence dramatically. Much of modern auction design concerns itself precisely with which format performs best when equivalence fails.

Bid Shading · The First-Price Equilibrium

Revenue equivalence gives us a shortcut for deriving equilibrium strategies. In a Vickrey auction with n bidders whose values are drawn uniformly from zero to one hundred, the expected payment by the winner equals the expected second-highest value. For the first-price auction to generate the same expected revenue, the equilibrium bid must be the expected value of the highest opponent's value, conditional on your value being the highest. With n symmetric bidders drawing from a uniform distribution on zero to v-bar, this works out to: b(v) = v · (n − 1) / n.

So with six bidders, each bidder shades their bid to five-sixths of their true value — a precise balance between the desire to win and the desire to profit, as Levin explained. This bid shading is the hallmark of first-price auctions: unlike in Vickrey auctions, you never bid your true value. You always bid less. But the shading is calibrated so that, on average, the seller receives exactly the same revenue as in a Vickrey auction.

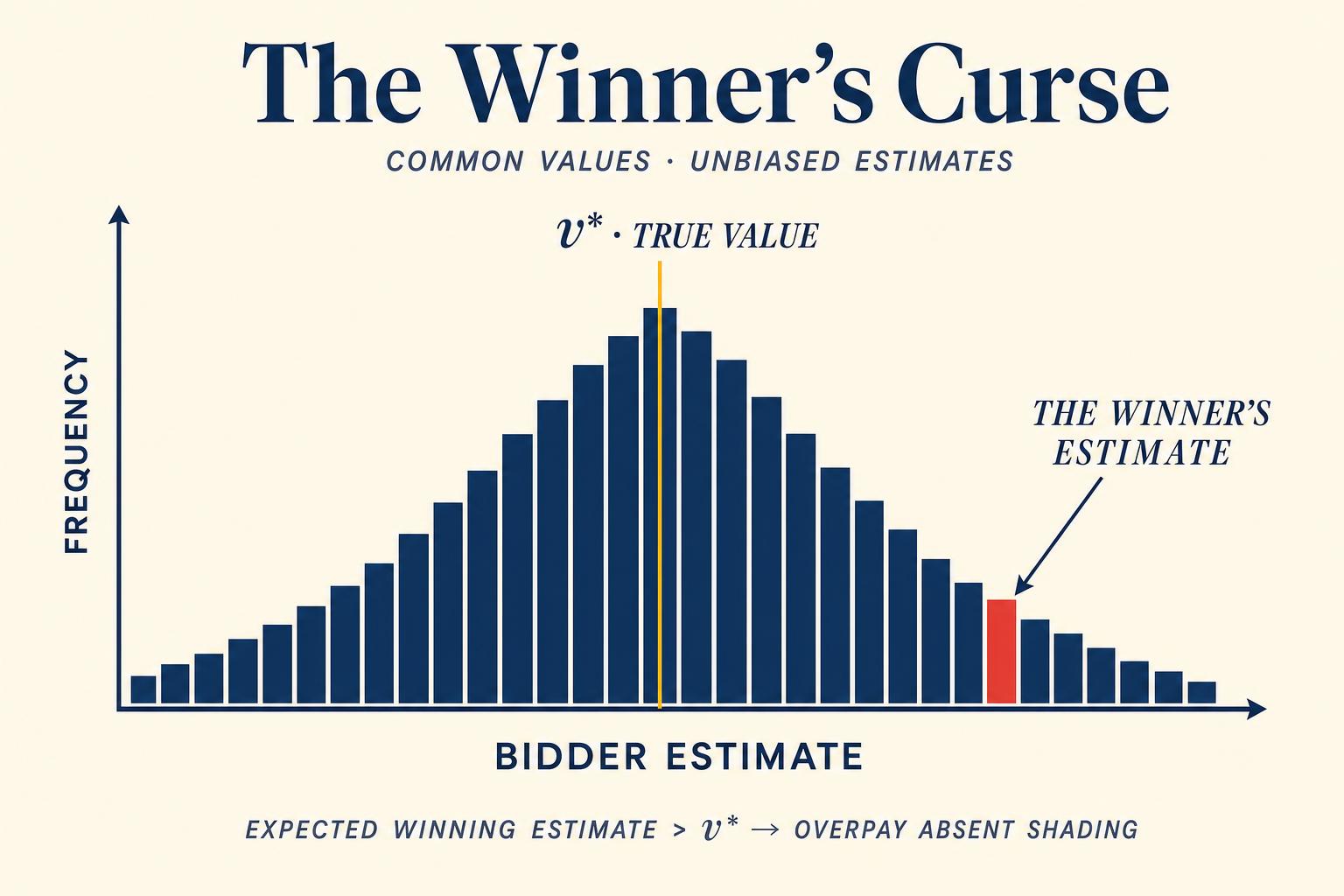

Common Values and the Winner's Curse

Everything we have discussed so far assumes private values: each bidder knows exactly how much the item is worth to them, and that value is unaffected by what others know. But many real-world auctions involve common values — the item has a single objective value that no bidder knows precisely. Oil drilling rights, mineral leases, Treasury bills, and corporate takeover targets all have common values: the oil field contains some amount of oil regardless of who wins the lease, but no bidder knows that amount for certain.

In a common-value auction, each bidder receives a noisy private estimate — a signal that is, on average, correct but subject to random error. Some bidders overestimate the true value; others underestimate it. Now consider who wins: in any standard auction, the winner is the bidder who bid the most, which typically means the bidder with the highest estimate. And the bidder with the highest estimate is, statistically, the bidder most likely to have overestimated the item's true value.

This is the winner's curse: the very act of winning tells you that your estimate was more optimistic than everyone else's, which is bad news about the item's true value, as Kagel and Levin documented extensively in two thousand two. If you bid naively — simply bidding based on your private estimate without accounting for this selection effect — you will systematically overpay.

Oil Leases · The First Documentation

The winner's curse was first documented in the context of the U-S Outer Continental Shelf oil lease auctions in the nineteen fifties and nineteen sixties. Companies bid billions of dollars for the right to drill in offshore tracts, basing their bids on geological surveys and seismic data — noisy estimates of how much oil lay beneath the seabed. In a celebrated nineteen seventy-one study, three Atlantic Richfield engineers — Capen, Clapp, and Campbell — showed that the companies winning these auctions were earning disastrously low returns on their investments. The winning companies had not accounted for the informational content of winning itself.

The logic is inescapable. Suppose ten companies each independently estimate the value of an oil tract. Even if every estimate is unbiased — correct on average — the highest of ten unbiased estimates will systematically exceed the true value. The winner, by definition holding the highest estimate, is the victim of statistical selection. To bid rationally, you must shade your bid downward to correct for this effect — not because you want to bluff, but because you are performing Bayesian updating.

Winning is Information

Recall that Bayesian updating means revising your beliefs in light of new information. In a common-value auction, winning is information. Specifically, winning tells you: "Your signal was the highest among all bidders." A rational bidder should ask: "What is the expected value of the item conditional on my signal being the highest?" This conditional expectation is always lower than the unconditional estimate, because the highest signal is biased upward, as the Royal Swedish Academy of Sciences explained in twenty twenty.

Robert Wilson formalized this insight in his foundational work on common-value auctions, showing how rational bidders in an equilibrium should discount their bids to account for the winner's curse. The remarkable finding from experimental work, however, is that most people fail to make this adjustment, even experienced professionals. In laboratory experiments, Kagel and Levin found persistent overbidding in common-value auctions — subjects consistently fell prey to the winner's curse, often losing money on average despite understanding the setup. The bias diminished with experience and feedback, but never fully disappeared.

Spectrum · From Theorem to Policy

For decades, auction theory was regarded as an intellectually beautiful but somewhat niche corner of economics. That changed in the early nineteen nineties, when the U-S Congress directed the Federal Communications Commission to allocate radio spectrum licenses by auction rather than by the administrative hearings and lotteries that had been used previously. The FCC faced an unprecedented design challenge: how to simultaneously sell thousands of interdependent licenses — for different geographic regions and frequency bands — to firms whose valuations depended on which combinations of licenses they could acquire, as Cramton described.

The FCC turned to a team of economists led by Paul Milgrom and Robert Wilson at Stanford. Drawing on three decades of auction theory, they designed the simultaneous multiple round auction, or S-M-R auction, a format in which all licenses are auctioned simultaneously over multiple rounds. In each round, bidders can place bids on any license. Prices rise incrementally, and activity rules require bidders to remain active on a specified number of licenses or lose future bidding eligibility. This rule prevents bidders from strategically holding back to observe others. The auction continues until no new bids are placed on any license, as Milgrom detailed in two thousand four.

The S-M-R design addressed several problems that simpler formats could not. Sequential auctions — selling licenses one at a time — would have exposed bidders to the "exposure problem": a firm might win License A at a high price, hoping to complement it with License B, only to lose License B and be stuck overpaying for a standalone license. Sealed-bid formats would have provided no price discovery, leaving bidders to guess wildly about competitive conditions. The S-M-R format's multiple rounds allowed gradual price discovery while its simultaneity protected against the exposure problem.

Results · A Hundred Billion Dollars

The results exceeded expectations. The first broadband PCS auction, the "C-block" auction of nineteen ninety-five to ninety-six, raised over ten billion dollars. Subsequent spectrum auctions in the United States, collectively, have generated over two hundred billion dollars in government revenue. Critically, efficiency was the primary design goal — ensuring licenses went to the firms that valued them most and could deploy wireless service most effectively. Cramton's early assessment found that the auctions were remarkably efficient, with licenses largely going to major carriers who could exploit geographic complementarities.

The model spread globally. Australia's spectrum authority, the ACMA, adopted auction-based allocation for its 4G and 5G spectrum assignments, adapting the S-M-R framework to local market conditions. The United Kingdom, Germany, India, and dozens of other countries followed suit, each tailoring auction formats to their regulatory environments while building on the same theoretical foundations.

The 2020 Nobel Prize

In October twenty twenty, the Royal Swedish Academy of Sciences awarded the Nobel Memorial Prize in Economic Sciences to Paul Milgrom and Robert Wilson "for improvements to auction theory and inventions of new auction formats." The prize committee highlighted three distinct contributions. Wilson developed the theoretical framework for common-value auctions, formalizing how rational bidders should account for the winner's curse. Milgrom generalized this to settings with both private and common value components, showing that auction formats which reveal more information to bidders tend to generate higher revenue — a result known as the linkage principle. And together, they designed the practical auction formats that governments use to allocate spectrum, landing slots, natural resources, and more.

The Nobel committee's citation captured something important about the relationship between theory and practice. Milgrom and Wilson did not merely analyze existing auctions; they created new ones. Their work is perhaps the most prominent example of mechanism design — the field, pioneered by Roger Myerson in nineteen eighty-one among others, that asks not "how do people behave in a given game?" but "how should we design the game to achieve a desired outcome?" Auction theory, in this sense, is game theory at its most applied and consequential.

Combinatorial Auctions and the Bigger Lesson

As auction design evolved, practitioners confronted complexities that the four standard formats could not handle. When bidders value combinations of items — as telecommunications firms value combinations of spectrum licenses — standard formats can lead to inefficient outcomes. A firm might need licenses in both Sydney and Melbourne to build a viable network; winning only one is nearly worthless. Combinatorial auctions allow bidders to submit bids on packages of items, ensuring that complementarities are reflected in the allocation. Milgrom developed several package bidding formats, including the combinatorial clock auction, which has been adopted for spectrum sales in multiple countries.

The design of these complex auctions draws on every concept in this chapter: dominant strategies to simplify bidder decision-making, revenue equivalence to benchmark expected revenue, common-value adjustments to mitigate the winner's curse, and mechanism design principles to ensure efficiency and discourage collusion.

Auction theory is game theory in its purest applied form. Every element we have studied — players with private information, strategic choices, payoff functions, equilibrium reasoning, dominance, and Bayesian updating — converges in the auction setting. The Vickrey auction's dominant strategy connects to our earlier work on dominance. The revenue equivalence theorem relies on equilibrium analysis. The winner's curse demands Bayesian reasoning. And mechanism design — the art of building the game itself — points forward to the broader questions of institutional design.

Perhaps most importantly, auction theory demonstrates that game-theoretic reasoning is not merely an academic exercise. The difference between a well-designed auction and a poorly designed one can be measured in billions of dollars of revenue, in the efficient or inefficient allocation of critical public resources, and in the success or failure of firms that stake their futures on the outcome. When Milgrom and Wilson sat down to design the FCC spectrum auction, they were not applying a metaphor. They were applying mathematics — the same mathematics you have been learning. Theory, meet practice.

Key Takeaways

- The four standard auction formats — English ascending, Dutch descending, first-price sealed-bid, and second-price sealed-bid or Vickrey — differ in their rules but are connected by deep strategic equivalences: English is equivalent to Vickrey, and Dutch is equivalent to first-price sealed-bid (Krishna, 2009; Levin, 2004).

- In a Vickrey auction, bidding your true valuation is a weakly dominant strategy (Vickrey, 1961). The proof uses the same dominance reasoning we've developed — overbidding risks negative surplus, underbidding risks missing profitable wins.

- The Revenue Equivalence Theorem shows that under standard assumptions — risk-neutral, independent private values, symmetric bidders, efficient allocation — all four formats yield the same expected revenue to the seller (Myerson, 1981; Milgrom, 2004).

- The winner's curse arises in common-value auctions: the winner, holding the highest estimate, has likely overestimated the item's true value (Capen, Clapp & Campbell, 1971; Kagel & Levin, 2002). Rational bidding requires Bayesian updating — conditioning your valuation on the information content of winning.

- Milgrom and Wilson's design of the FCC spectrum auctions translated auction theory into policy, generating over two hundred billion dollars globally and earning the twenty twenty Nobel Prize in Economics (Cramton, 1997; Royal Swedish Academy of Sciences, 2020).

- Mechanism design — the art of engineering the rules of strategic interaction — represents game theory's most powerful applied frontier, with auctions as its signature success story.

Auctions are one specific class of mechanism — a game designed to achieve a goal. In Evolution's Strategists, we broaden the lens to evolutionary game theory: how strategic equilibria emerge without conscious reasoning, why some traits and behaviours are evolutionarily stable, and what bower birds, hawks, doves, and bacteria can teach us about Nash equilibrium in nature.

References

Capen, E. C., Clapp, R. V., & Campbell, W. M. (1971). Competitive bidding in high-risk situations. Journal of Petroleum Technology, 23(6), 641–653.

Cramton, P. (1997). The FCC spectrum auctions: An early assessment. Journal of Economics & Management Strategy, 6(3), 431–495.

Kagel, J. H., & Levin, D. (2002). Common Value Auctions and the Winner's Curse. Princeton University Press.

Krishna, V. (2009). Auction Theory (2nd ed.). Academic Press.

Levin, J. (2004). Auction theory. Lecture notes, Stanford University.

Milgrom, P. (2004). Putting Auction Theory to Work. Cambridge University Press.

Myerson, R. B. (1981). Optimal auction design. Mathematics of Operations Research, 6(1), 58–73.

Royal Swedish Academy of Sciences. (2020). Scientific background on the Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2020: Improvements to auction theory and inventions of new auction formats.

Vickrey, W. (1961). Counterspeculation, auctions, and competitive sealed tenders. The Journal of Finance, 16(1), 8–37.